管理会計最終回として、経営戦略と管理会計の関係について話しています。

0:50 前回の振り返り、1:45 経営戦略と管理会計、4:50 Strategy Map、24:40 Balanced Scorecard、29:21 Action Plan

前回の振り返り

- 管理会計は、社内の動きをお金の観点で測定、分析できる手法

- コストの把握方法はTD-ABC、時間駆動型活動原価計算。

- Performanceの測定、利益分析の観点として、Whale curve、Customer Life Time Value、Variance Analysis

今回のテーマ:管理会計を経営戦略にどう生かすか

- 管理会計は戦略の実行段階でとても重要。Planningだけじゃなく実行して初めて戦略は意味がある!

- ModelはStrategy Map + Balanced Scorecard + Action Planの3つで構成

- Strategy Map と Balanced Scorecardの組合せでStrategyを表現し、Action Planを策定。Action Planの達成度を管理会計の各種分析手法で解析。

- “If you can’t measure it, you can’t manage it. If you can’t manage it, you can’t improve it.” – Peter Drucker

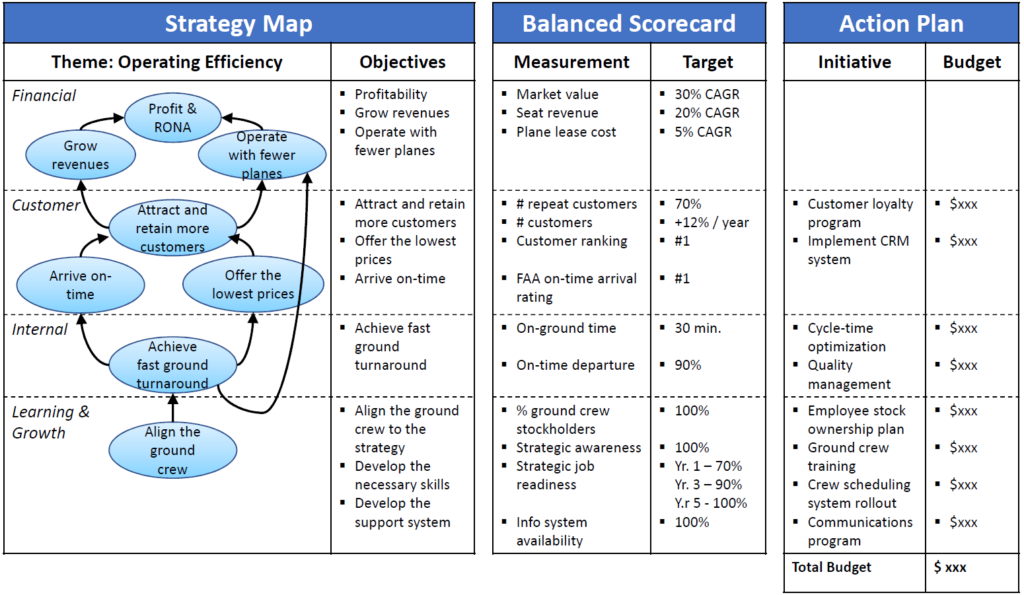

Strategy Map:戦略的目標の構造化手法

- 4つの観点で戦略的目標strategic objectivesを分解し、4. Learning & Growth から 1. tangible outcomesへの貢献経路を矢印で表現

- Financial:tangible outcomesを定義

- Customer:valueのsourceを定義

- Process:cusotmerとstakeholderに価値を提供する社内プロセスを定義

- Learning & Growth:必要なintangible assetを定義

- ObjectivesのGuidelines

- verb + nounで簡潔にエッセンスを記述

例:Good: Provide customer-focused solutions, Bad: customer satisfaction - プロジェクトを含めないようにする

例:Good: Understand customer behavior, Bad: Implement Customer Relationship Management system - 1つのmapにstrategic objectivesは15-25個程度。financialは1/5以内に抑え、40%ぐらいを社内プロセスに。

- verb + nounで簡潔にエッセンスを記述

- システムダイナミクスみたい!

Kaplan and Norton, “Strategy Maps: Converting Intangible Assets into Tangible Outcomes,” 2004, p.53, partially modified.

Balanced Scorecard:戦略実行時の具体的な目標を記述

- 各Strategic Objectivesに対応する、測定量とそのtargetの対応表。測定量とtargetは1:1。

- 一つのstrategic objectivesに対して測定量を1個か2個設定 => 一つのmap全体で~30個程度

- 例:利益率10%増、ランキング1位

Action Plan:戦略実行時の具体的なプロジェクトを記述

- Balanced Scorecardのtargetを達成するためのinitiative/projectと予算の対応表

- 例:Itinitative: CRM system、予算: $10MM

Comments are closed, but trackbacks and pingbacks are open.